Impact of Lockdowns on Customer Attitudes

Following a year of restrictions impacting collectors we take a deep dive into changes in consumer attitudes and shopping habits.

Customer Economic Outlook

Get Worse

Get Better

"Paradoxically I have been better off without commuting costs and buying lunches at the office" Male 55-64

Customer Health

Most customers say their health has been impacted since lockdown began last year.

0

Claim Physical Health Impacted

0

Claim Mental Health Impacted

Source: Nectar Omnibus Feb 2021

Lockdown Impact

Lockdowns have impacted different groups in different ways. The lack of social interaction was the main concern of Nectar collectors over the last year – particularly impacting females. Younger collectors were more likely to report isolation or personal finances amongst their concerns.

As discussed in our article 2021 Customer mindset: Health, our collectors have become less focused on exercise throughout the year, dropping from 62% reporting doing exercise twice a week in May 2020 to only 53% in Jan 2021. The importance of this issue is reflected in the volume of collectors reporting that lack of motivation or exercise are concerns.

Comfort with Travelling

Following a relative high in comfort with holiday planning in the summer, there was a sustained decline as the second wave took hold and new variants emerged. The government’s roadmap for opening international travel has meant more Nectar customers feel comfortable with booking holidays in March than have done for many months.

Somewhat uncomfortable/Not comfortable at all

Very comfortable/Somewhat comfortable

"I'm planning a beach holiday but not before September 2021" Female 35-44

Shopping Preferences

The majority of customers agree that grocery shopping is best in-store, with over half saying that they prefer shopping both online and in-store. However, physical stores remain important, as very few customers want to move online for all of their grocery shopping needs.

Grocers who optimise their multi-channel offering will be best placed to serve customer needs going forwards.

Following the relaxation of rules, most customers would prefer to shop for products in-store, especially groceries and DIY/gardening. However, preference is less clear for Toys and Electronics, which could prove challenging for bricks and mortar retailers in these industries. 25-34 year olds are the least likely to move back to in-store shopping, with only 34% preferring to do their Electronics shopping offline in future.

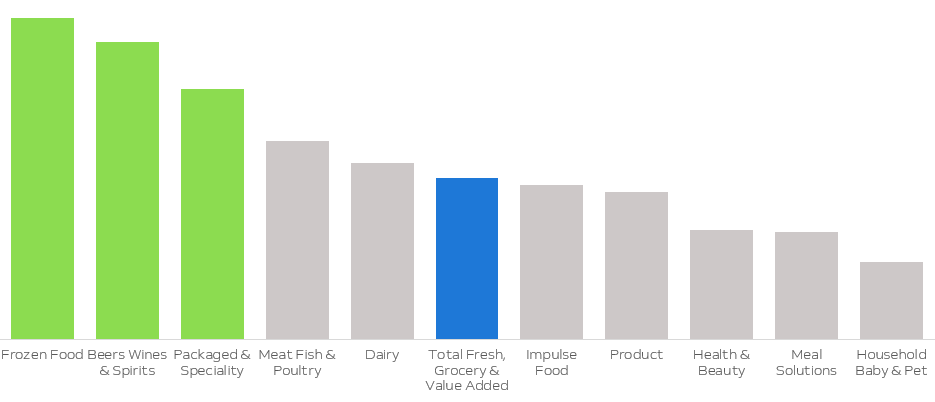

Sales Category Shift

As mentioned in our 2020 Year in Review, Sainsbury’s customers have bought far more long lasting foods since lockdown began. While making fewer shops, it has been important to have products that last longer, such as frozen foods and packaged goods.

The closure of bars and pubs for most of the year has shifted Beer, Wine and Spirit purchasing to part of customers’ grocery shops.

YoY Category Sales Growth

Source: Sainsbury’s sales data